{kind=link}

Think the Fed’s call this week won’t touch your mortgage?

Think again.

Markets start moving the moment the Fed speaks, and lenders often reprice rates in 24 to 72 hours.

That can shift posted mortgage rates, affect locked loans, and change payments or even close dates for buyers finishing a deal.

This post lays out how the Fed decision moves Treasuries and mortgage-backed securities, what that means for locks and closings, and the practical steps buyers and sellers should take in the next 48 to 72 hours.

Immediate Impact of This Week’s Fed Decision on Mortgage Rates and Closings

Markets price in a Fed decision the second Jerome Powell starts his press conference. Sometimes before he finishes answering question one. Treasury yields and mortgage-backed securities start trading right away. Lenders reprice their rate sheets within 24 to 72 hours, which means you can see different numbers by the next business day.

A typical 25 basis point Fed hike usually pushes mortgage rates up somewhere between 5 and 30 basis points (0.05% to 0.30%) in the days right after. A 25 to 50 basis point cut can bring mortgage rates down 10 to 40 basis points over several days to weeks, though timing varies depending on whether the move was expected or came as a surprise. If everyone saw the decision coming, actual mortgage movement is usually smaller because bond traders already repositioned weeks earlier.

For borrowers mid-transaction, locked rates stay valid until the lock expires. That’s commonly 30, 45, or 60 days from when you signed the lock agreement. If you haven’t locked yet and rates jump, you’ll pay the new, higher rate at closing. Lock extensions typically cost 0.125% to 0.50% of the loan amount per 30-day period, which translates to $500 to $2,000 on a $400,000 loan. Rate spikes can also push debt-to-income ratios over underwriting thresholds, which can delay or kill a closing if the lender has to requalify you at a higher payment.

If you’re closing soon, here’s what the Fed decision immediately affects:

- Lock protection – Your locked rate stands firm until expiration. Verify the exact date and extension cost in dollars today.

- Float-down options – Many lenders offer a one-time float-down if rates drop 25 to 50 basis points. Confirm the trigger threshold and any fees.

- Closing-week risks – If appraisal or underwriting delays push you past the lock window, you may need to re-lock at the new market rate or pay to extend.

- Payment changes – A 0.25% rate increase on a $400,000 loan adds roughly $60 to $70 per month. A 0.50% increase adds about $120 to $140.

- Lender verification – Call or email your lender within 48 hours to confirm whether they’ve repriced, whether your lock is still active, and what happens if you miss the closing date.

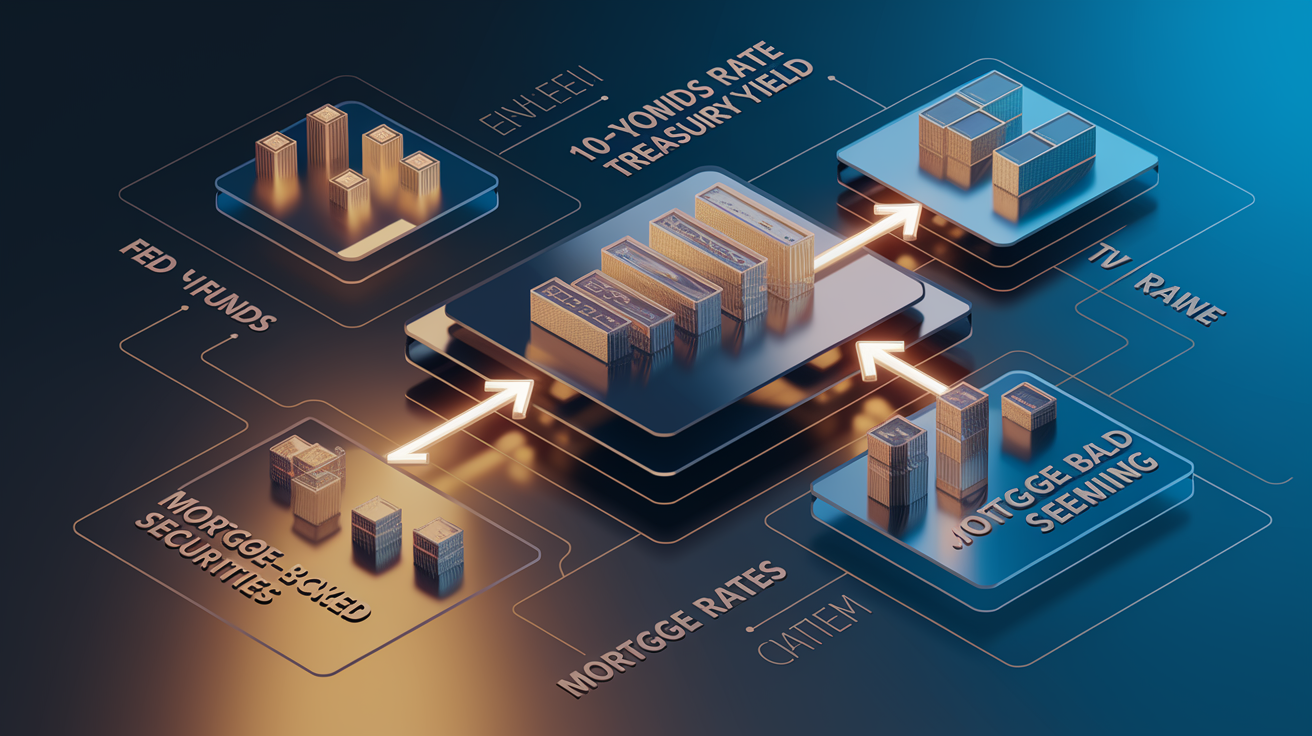

How Fed Policy Mechanically Moves Mortgage Rates

The Federal Reserve sets the federal funds target rate, which governs overnight lending between banks. It doesn’t directly set the interest rate on a 30-year fixed mortgage. Mortgage rates follow the bond market, especially the 10-year Treasury yield, which typically runs 150 to 200 basis points (1.5% to 2.0%) below the average 30-year mortgage rate. When the Fed raises or cuts the funds rate, Treasury yields react to the policy signal and the forward economic outlook the Fed describes. Those Treasury moves then push mortgage-backed securities prices up or down, and lenders reprice accordingly.

The table below shows the chain of influence from the Fed’s decision to the rate you see on a lender’s quote.

| Market Component | What Moves It | Impact on Mortgage Rates |

|---|---|---|

| Fed Funds Rate | FOMC vote and policy statement | Indirect; signals inflation/growth expectations and shifts Treasury demand |

| 10-Year Treasury Yield | Bond-trader expectations of Fed path, inflation, and economic data | Direct; mortgage rates typically move in the same direction within hours to days |

| Mortgage-Backed Securities (MBS) Demand | Investor appetite for mortgage bonds relative to Treasuries | Direct; higher MBS prices lower mortgage rates; lower prices raise rates |

| Economic Data (CPI, Jobs, GDP) | Releases between Fed meetings | Indirect; shape market expectations and drive yield volatility week to week |

Expected Mortgage Rate Scenarios After a Fed Hike, Hold, or Cut

How mortgage rates move depends on what the Fed does and how surprising the action is. The three main scenarios play out differently in timing, magnitude, and market psychology.

1. Fed raises rates (+25 basis points): Mortgage rates typically rise 5 to 30 basis points within 24 to 72 hours. The increase is smaller if traders already priced the hike into Treasury yields weeks earlier. The increase is larger if the Fed signals more hikes to come or if the accompanying statement sounds more hawkish than expected. Borrowers see higher posted rates quickly. Buyers with floating locks face immediate repricing risk.

2. Fed holds rates steady: Mortgage rates usually move very little in the first 24 hours unless the Fed’s forward guidance or “dot plot” projections shift expectations. If the Fed signals future cuts, Treasury yields can fall and mortgage rates can drift lower over days. If the Fed hints at keeping rates higher for longer, yields can tick up and mortgage rates can edge higher. The hold scenario often creates a wait-and-see dynamic where buyers and sellers pause to see what economic data does next.

3. Fed cuts rates (−25 to −50 basis points): Mortgage rates often fall 10 to 40 basis points over several days to a few weeks. The lag can be longer than in a hike scenario because lenders sometimes delay repricing downward to protect profit margins. If the cut was widely expected, much of the mortgage-rate decline may have already happened before the announcement. If the cut is a surprise or the Fed signals aggressive easing ahead, mortgage rates can drop more sharply and refinance applications typically surge within a week.

Historical Examples Showing How Fed Moves Have Shifted Mortgage Rates

Past Fed cycles show how policy changes translate into real mortgage-rate movement and help set realistic expectations for the next few weeks. The timing and magnitude vary, but the patterns hold.

In March 2020, the Fed slashed the funds rate to 0.00–0.25% in an emergency response to pandemic lockdowns and launched massive Treasury and MBS buying. Within weeks, the average 30-year fixed mortgage rate fell into the mid-2% range. Briefly touching lows around 2.65% by early 2021. The combination of zero policy rates and quantitative easing flooded the bond market with liquidity, compressing mortgage spreads to unusually tight levels.

The 2022 hiking cycle moved in the opposite direction. The Fed raised the funds rate by a cumulative 4.25 percentage points across the year, pushing the target from near zero to a range of 4.25–4.50% by year-end. Average 30-year mortgage rates climbed from roughly 3.2% in January 2022 to a peak near 7.0% by late fall. The magnitude was larger than the Fed’s policy move because inflation fears, MBS selling, and recession concerns drove Treasury yields sharply higher.

Key historical reference points:

- 2020–2021: Fed at 0.00–0.25%, mortgage rates in the low-to-mid 2% range; record refinance volume and home-price acceleration.

- 2022 hiking cycle: Fed raised 4.25 percentage points total; mortgage rates rose from ~3.2% to ~7.0%; home sales and refinance activity collapsed.

- 2023 stabilization: Fed held at 5.25–5.50%; mortgage rates oscillated in the mid-6% to low-7% range as Treasury yields reacted to inflation and jobs data.

- 2024–2025 decline: Fed cut in late 2024; mortgage rates dropped from 6.91% in January 2025 to 6.15% by December; rate briefly dipped below 6.0% in February for the first time in years.

How This Week’s Fed Decision Affects Buyers With Pending Closings

If you’re mid-transaction, the Fed’s move this week can change your rate, payment, and even whether your loan clears underwriting. The size of the impact depends on your lock status, closing date, and how much rates actually move in the bond market.

Borrowers with a rate lock are protected until the lock expires. Common lock periods are 30, 45, or 60 days. If you locked at 6.5% for 45 days and the Fed hikes rates this week, you still close at 6.5%. Assuming you close before the lock window ends. If your closing gets delayed past the expiration date, you’ll need to extend the lock or re-lock at the current market rate. Extensions typically cost 0.125% to 0.50% of the loan amount per 30 days. On a $400,000 loan, that’s $500 to $2,000. Some lenders offer a float-down feature that allows one repricing if rates fall by a set threshold, often 25 to 50 basis points. Verify in writing whether your lock includes a float-down, what the trigger is, and whether there’s a fee.

Borrowers who haven’t locked yet face immediate repricing risk. If the Fed moves rates and lenders reprice within 24 to 72 hours, you could lock at a rate significantly different from what you saw last week. If you’re closing within 14 days, locking immediately is usually the safer play. If you’re closing in 15 to 45 days, weigh the risk of rising rates against the chance of a decline and decide whether to float or lock now. If your closing is more than 45 days out, floating is riskier. Consider a lock with an extension option or a product built for longer timelines.

Specific items to verify and actions to take if you’re closing soon:

- Lock expiration date – Get the exact date in writing. Don’t rely on verbal estimates or rough “30-day” language.

- Float-down rules – Confirm the basis-point threshold, whether it’s one-time or repeatable, and any associated fee.

- Extension fees – Ask for the per-30-day cost in both percentage points and dollars. Compare across lenders if you’re still shopping.

- Appraisal and underwriting delays – If your appraisal or title work is late, you risk missing the lock window. Push for completion and get status updates daily.

- Lender requalification triggers – If your transaction stretches beyond 30 to 45 days or your lock expires, some lenders re-run credit and income checks. Rising rates can push your debt-to-income ratio over the threshold.

- Seller negotiation – If rates spike and your payment increases materially, discuss whether the seller will extend the closing date or offer a credit to keep the deal alive.

Effects on Loan Types: Fixed-Rate, Adjustable-Rate, FHA, VA, and Jumbo Mortgages

Not all mortgage products react the same way or on the same timeline when the Fed moves. The sensitivity depends on the underlying index, the lender’s funding model, and the secondary-market appetite for different loan types.

1. Fixed-rate mortgages (30-year and 15-year): These move in step with the 10-year Treasury and the MBS market. When the Fed hikes or cuts and Treasury yields adjust, fixed-rate mortgage pricing follows within 24 to 72 hours. The 15-year fixed usually tracks slightly lower than the 30-year because it’s closer in duration to intermediate bonds. Fixed-rate loans offer the most protection against future rate volatility, but they also lock you into the current market level.

2. Adjustable-rate mortgages (ARMs): Initial teaser rates on ARMs are often tied to short-term benchmarks like SOFR (Secured Overnight Financing Rate), which moves more quickly in response to Fed policy. When the Fed raises the funds rate, SOFR usually rises within days, and new ARM quotes can reprice faster than fixed-rate loans. After the initial fixed period (commonly 5, 7, or 10 years), the rate adjusts periodically based on the index plus a margin. If you’re in an ARM and the Fed is hiking, expect your adjustment to move up when the reset date arrives.

3. FHA and VA loans: These government-backed products move in line with the broader mortgage market but can lag slightly because of the guaranty structure and the specialized MBS pools (Ginnie Mae) that fund them. Lenders price FHA and VA loans based on their bond-market exposure, so a Fed decision affects them indirectly through Treasury and MBS movements. Pricing can be more volatile if investor demand for Ginnie Mae securities shifts.

4. Jumbo mortgages: Jumbo loans (above conforming limits, currently $806,500 in most areas for 2025) aren’t backed by Fannie Mae or Freddie Mac, so they trade on portfolio or private-label MBS markets. Jumbo pricing is especially sensitive to liquidity and investor risk appetite. When the Fed tightens and bond-market volatility spikes, jumbo rates often rise faster and farther than conforming rates. When the Fed cuts and liquidity improves, jumbo spreads can tighten and rates can fall more sharply.

How Fed Rate Changes Influence Monthly Payments and Buying Power

A seemingly small shift in mortgage rates translates into real monthly-payment changes and can materially shrink or expand how much home you can afford. The math is straightforward, but the affordability impact compounds when you layer in property taxes, insurance, and debt-to-income limits.

A 0.25% (25 basis point) increase in the interest rate on a $400,000, 30-year fixed loan raises the monthly principal and interest payment by roughly $60 to $70. A 0.50% increase adds about $120 to $140 per month. A full 1.0% rate jump can increase the payment by $240 to $280. Those differences look modest in isolation, but lenders qualify you based on a debt-to-income ratio, commonly capping total monthly debt (mortgage, car, credit cards, student loans) at 43% to 50% of gross income. A $100 monthly increase can push you over the limit and either force you to buy a less expensive home or disqualify you entirely.

| Rate Change | New Approx. Monthly Payment (P&I on $400,000 loan) | Impact on Buying Power |

|---|---|---|

| +0.25% | +$60–$70/month | Reduces maximum loan by roughly $10,000–$12,000 at typical DTI limits |

| +0.50% | +$120–$140/month | Reduces maximum loan by roughly $20,000–$25,000 |

| +1.00% | +$240–$280/month | Reduces maximum loan by roughly $40,000–$50,000 |

Higher rates also cool buyer competition, which can moderate home-price appreciation or even push prices down in rate-sensitive markets. Lower rates increase buying power, which tends to heat up bidding and push prices higher. The interplay between rate moves and price moves is why a Fed decision this week can reshape the entire negotiating landscape for buyers and sellers within a matter of days.

Practical Steps Homebuyers Should Take in the First 48 Hours After the Fed Decision

The window immediately after the Fed announcement is when you have the most leverage to lock a rate, confirm terms, or pivot your strategy before lenders fully reprice and the market settles into a new range.

1. Call or email your lender within 24 hours to confirm whether they’ve repriced their rate sheet. Ask for the current 30-year fixed rate, any points or fees, and whether your existing lock (if you have one) remains valid.

2. Verify your lock expiration date in writing. Get the exact calendar date, not a vague “30 days from application.” Confirm what happens if you miss that date. Extension cost, automatic re-lock at market, or cancellation.

3. If you’re floating, ask for the current lock cost and float-down provisions. Confirm the basis-point threshold for a float-down (commonly 25 to 50 bps), whether it’s one-time only, and any fees. Get the terms in an email or addendum.

4. Request a revised Loan Estimate if rates or fees have changed materially. Federal rules require lenders to provide an updated disclosure if key terms shift. Use the revised LE to compare the new payment, cash-to-close, and APR against your budget.

5. Run a debt-to-income calculation at the new rate. Add your estimated mortgage payment (principal, interest, taxes, insurance, HOA) to your other monthly debts, divide by your gross monthly income, and check whether you’re still under the lender’s DTI limit (typically 43%–50%). If you’re close to the edge, consider locking immediately or reducing other debts.

6. Coordinate with your real estate agent, title company, and seller to accelerate any outstanding conditions. Appraisal, inspection, document uploads, and title clearance can all delay closing. The faster you complete these, the less risk you face of missing your lock window.

Outlook: What to Watch in Markets After This Week’s Fed Move

The Fed decision is one data point in a continuous stream of economic releases and market reactions. Mortgage rates will continue to move in the days and weeks after the announcement, driven by fresh inflation data, jobs reports, Treasury-auction results, and updated Fed commentary.

The Consumer Price Index (CPI) and Producer Price Index (PPI) releases are the most immediate inflation signals. If inflation runs hotter than expected after a Fed cut, Treasury yields can reverse and push mortgage rates back up. If inflation cools after a Fed hold or hike, yields can fall and mortgage rates can drift lower even without another Fed move.

Key items to monitor over the next several weeks:

- CPI and core inflation data – Monthly releases can move Treasury yields 10 to 30 basis points in a single day. Mortgage rates follow within 24 to 72 hours.

- Jobs report (nonfarm payrolls and unemployment rate) – Strong employment supports higher rates. Weak jobs data can push rates down as recession fears grow.

- 10-year Treasury yield movement – Watch the daily trend. A sustained 20 to 30 basis point move in Treasuries usually translates into a mortgage-rate shift of similar size.

- Next Fed meeting expectations – Market pricing for the next FOMC decision (visible in fed funds futures) shapes Treasury positioning. If traders start pricing a surprise cut or hike, mortgage rates will move ahead of the actual meeting.

Final Words

The Fed just spoke, and markets moved, with mortgage pricing shifting within hours. Lenders typically reprice in 24 to 72 hours.

We covered the mechanics (Treasuries to MBS to lender pricing), scenario outcomes (hike, hold, cut), historical examples, loan-type differences, and the specific risks for buyers with pending closings.

If you’re wondering how a Fed decision this week affects mortgage rates and closings, confirm your lock, ask about float-downs or extension costs, and watch Treasury yields plus CPI and jobs reports. Quick, practical checks usually protect most deals, so stay proactive and you’ll keep options open.

FAQ

Q: Will mortgage rates go down if the Fed cuts rates?

A: Mortgage rates will often fall after a Fed cut, but not automatically; a 25–50 bps Fed cut typically translates to about a -10 to -40 bps mortgage drop over days–weeks, driven by Treasuries and MBS.

Q: What is the 3 7 3 rule in mortgage?

A: The 3 7 3 rule in mortgage isn’t a universal industry standard; meanings vary by region or lender, so ask your loan officer or share the context for a specific, clear definition.

Q: Is there going to be a housing crash in 2026?

A: A housing crash in 2026 is not certain; current signals are mixed. Watch inventory, price cuts, unemployment, and mortgage rates—any broad, sharp deterioration would change the outlook.

Q: Are mortgage rates expected to drop to 5%?

A: Mortgage rates dropping to 5% is possible if Treasuries fall and the Fed eases; typical Fed cuts can shave -10 to -40 bps, so reaching 5% depends on starting levels and broader bond moves.