{kind=link}

Are builders quietly forcing resale prices lower by hiding big discounts inside new-home incentives?

Recent data show incentive-heavy new sales can cut net-effective prices by roughly 3% to 5%, changing buyer math even when list prices don’t move.

That matters because buyers compare monthly payments and cash needed, not sticker price; rate buydowns and upgrade credits often make new homes look like better value.

The result: faster buyer traffic for new builds, longer days on market, and measurable downward pressure on nearby resale prices as appraisers use incentive-laden closings as comparables.

How Builder Incentives Directly Influence Resale Home Prices

Builder incentives reshape what buyers actually pay without touching the sticker price. Q4 2025 numbers tell the story: median new single-family home sold for $405,300, while the median existing home went for $414,900. Existing homes have been priced above new construction in 5 of the last 7 quarters since Q2 2024. That’s a sustained flip from how things used to work. When builders stack mortgage-rate buydowns, closing-cost credits, and upgrade packages on top of already competitive pricing, the real purchase cost of a new home can drop 3% to 5% below what’s on the sign. Buyers start weighing monthly payments and actual cash needed against list price alone.

More than two-thirds of new-home communities now offer mortgage-rate buydowns. On a $400,000 mortgage, a 2-point rate reduction (say, from 6.0% to 4.0%) cuts monthly principal and interest by about $489. That’s nearly $5,900 saved in the first year. When a buyer can lock in a lower payment plus reduced closing costs on a brand-new home priced near or even below a comparable resale property, demand shifts. Sellers in those neighborhoods see slower traffic, longer days on market, and pressure to either drop their asking price or match what the builder’s offering through their own concessions.

Appraisers pull recent closed sales when they value homes. When new-build sales carry significant concessions, those transactions become comparables. Within one to three quarters, incentive-heavy new-home closings start showing up in resale appraisal reports, compressing value benchmarks in nearby resale neighborhoods. The shift’s measurable. If a cluster of new builds closes at net-effective prices 3% to 5% below their list figures, appraisers adjust their grids. Resale sellers find their appraisals coming in lower than expected, even when their list price seemed competitive against published new-home prices.

Five ways builder incentives pull demand from resale properties and trigger pricing pressure:

- Payment-capacity expansion. Rate buydowns and closing-cost credits boost a buyer’s effective purchasing power, letting them afford a higher-priced or better-located new home for the same monthly outlay. That pulls them out of the resale pool.

- Perceived value gap. Included upgrades like countertops, flooring, appliances create a tangible feature advantage. Resale homes have to counter with upgrades or price cuts.

- Inventory substitution. Quick-move-in new homes compete directly with resale turnkey inventory, offering a finished product with less negotiation friction and no repair contingencies.

- Comparable-sales compression. As incentive-laden new sales close, they set lower price benchmarks that appraisers use when valuing nearby resale properties. That shrinks the supportable list price for existing homes.

- Marketing velocity. Builder incentive campaigns often feature aggressive digital and on-site promotion, increasing buyer awareness and foot traffic to new developments while pulling attention from resale listings in the same market.

Understanding the Types of Builder Incentives That Compete With Resale Homes

Builders structure incentives to improve the buyer’s deal without dropping the headline sale price. Keeping the base price stable protects community comparable values and future lot pricing, but the effective discount still changes the buyer’s math. Incentive packages commonly range from $10,000 to $25,000. That’s 2% to 5% of the purchase price on a typical $400,000 to $500,000 new home. These offers are usually time-sensitive, vary by community and home type. Many require the buyer to use the builder’s preferred lender to capture the full benefit.

Four main builder incentive types:

- Mortgage-rate buydowns. The builder pays upfront points to reduce the buyer’s interest rate, either permanently or for a temporary period (like 2–1 or 1–0 buydowns). This lowers monthly payments immediately and is one of the most visible and psychologically powerful incentives.

- Closing-cost assistance. The builder covers part or all of the buyer’s closing fees (title, escrow, origination), reducing the cash required at closing and making the transaction more accessible for buyers with limited reserves.

- Design-center and upgrade credits. Buyers get a dollar allowance or specific upgrades (premium countertops, flooring, appliances, smart-home packages) included in the base price. Adds perceived value without changing the contract price.

- Price reductions on inventory or quick-move-in homes. Builders discount completed or near-complete homes to clear inventory quickly, avoiding carrying costs and freeing capital for the next phase. These discounts are often steeper than pre-construction incentives.

Resale sellers typically offer price concessions or limited closing-cost help. But they rarely have the capital or structured programs to fund multi-point rate buydowns or deliver $15,000 upgrade packages at closing. A buyer comparing a $425,000 resale home with modest seller-paid closing costs against a $430,000 new home with a 2-point rate buydown, $10,000 in upgrades, and $5,000 in closing help will often see the new build as the better deal. Even though the list price is higher. The resale home’s advantages (lot maturity, location nuances, lower HOA fees) become secondary unless the seller adjusts price or adds equivalent concessions. In markets where new-home incentives are widespread and visible, resale homes have to compete on net-effective value, not list price alone.

Market Conditions That Cause Builders to Increase Incentives and How Those Conditions Affect Resale Prices

Builders ramp up incentives when carrying costs on unsold inventory become a drag on capital and when buyer demand softens. At the end of August 2025, new-home inventory stood at roughly 490,000 units, about 4% higher than the same time in 2024. Sales of new single-family homes remained “relatively mild” through 2025, as higher mortgage rates and affordability constraints kept buyers on the sidelines. Every unsold completed home racks up financing, property taxes, insurance, and maintenance costs. Quick-move-in and inventory homes generate the most aggressive incentives because moving those units fast reduces carrying costs and frees up working capital for the next construction phase.

When inventory builds and absorption slows, the competitive pressure on resale homes gets intense. Builders with scale and capital can deploy rate buydowns, upgrade packages, and closing-cost help in a coordinated way across multiple communities. That creates a wave of attractive offers that pull buyer attention and traffic. Resale sellers in the same school district or price band suddenly face longer days on market, fewer showings, and buyers who reference the builder’s package when making lower offers. The result is localized price compression. Resale list prices stagnate or fall, seller concessions rise, and transaction velocity slows until either the builder’s inventory clears or resale sellers adjust their pricing to match the net-effective cost of the new competition.

Regional Differences in Incentive Impact and Resale Price Pressure

The magnitude of incentive-driven resale pressure varies sharply by region. It’s shaped by the existing price relationship between new and resale homes and the concentration of new construction. In Q4 2025, regional median prices showed wide divergence in the new-versus-existing premium.

| Region | New Median | Existing Median | Premium (New vs Existing) |

|---|---|---|---|

| Northeast | $799,000 | $515,900 | +$283,100 (new > existing) |

| Midwest | $377,900 | $317,200 | +$60,700 (new > existing) |

| West | $557,100 | $623,800 | −$66,700 (existing > new) |

| South | $366,100 | $367,200 | −$1,100 (existing > new) |

In the South and West, where existing homes are already priced at or above new homes, builder incentives create immediate and visible pressure on resale values. A $366,100 median new home in the South with $15,000 in combined incentives becomes a $351,100 net-effective purchase, undercutting the $367,200 existing median by a meaningful margin. Resale sellers in those markets have to adjust quickly or risk extended days on market and appraisal gaps. In the West, the $66,700 existing-home premium means resale homes start at a structural disadvantage. When builders layer incentives on top of already lower new-home pricing, the competitive gap widens.

In the Northeast and Midwest, where new homes carry a premium over existing homes, the incentive impact is more nuanced. The Northeast’s $283,100 new-home premium suggests that new construction serves a different buyer segment or product type. Moderate incentives may not move the median resale price. But within specific subdivisions or school districts where new and existing homes compete more directly, localized resale pressure can still be significant. The Midwest’s smaller $60,700 premium means that even moderate builder incentives can erase much of the new-home price advantage, pulling buyers from resale inventory and creating measurable downward pressure on resale list prices and seller negotiating power.

How Incentives Influence Comparable Sales Data and Appraisals for Resale Homes

Builders typically keep their base contract prices stable to protect the perceived value of future phases and unsold lots. But the incentives they offer reduce the buyer’s net cost. Appraisers are trained to identify and adjust for seller concessions, but the treatment of builder incentives varies depending on how they’re structured and disclosed. When a builder funds a mortgage-rate buydown or provides closing-cost assistance, those costs may be captured in the settlement statement but not always reflected in the reported sale price. Over time, as incentive-heavy new-home sales close and appear in the MLS or public records, they become part of the comparable-sales pool that appraisers use to value nearby resale homes.

The lag between when incentives are offered and when they affect resale appraisals is typically one to three quarters. A wave of builder promotions in Q1 will start to show up as closed comparable sales in Q2 and Q3. Appraisers pulling six-month lookback windows will incorporate those transactions. If several new-build sales in a neighborhood closed at effective net prices 3% to 5% below their list figures, the appraisal grid reflects that lower pricing. Even if the resale seller’s list price was based on older, higher comps.

Three ways appraisers adjust for builder incentives:

- Net-price adjustment. When closing statements show significant seller-paid costs or credits, appraisers may adjust the comparable sale price downward to reflect the net amount the buyer effectively paid.

- Concession cap enforcement. Lenders often limit seller concessions to a percentage of the sale price (commonly 3% to 6% depending on loan type). Incentives that fall within those caps may be treated as normal market practice. Those that exceed them can trigger further scrutiny or downward adjustments.

- Market-condition trends. Appraisers note increasing prevalence of incentives as a market-condition factor, which can justify lower valuations across a neighborhood if the trend is widespread and sustained.

Resale sellers face appraisal gap risk when their accepted contract price is based on older comps that didn’t reflect recent builder concessions. A buyer’s lender orders an appraisal that pulls the latest closed sales, including several incentive-heavy new builds, and the appraised value comes in below the contract price. The deal then requires a price renegotiation, additional buyer cash, or seller concessions to close. All of which erode the seller’s net proceeds and reinforce downward price momentum. The timeframe for this effect is measurable. Within one to three quarters of a sustained builder incentive campaign, resale appraisals in competing neighborhoods typically reflect the lower net-effective pricing, forcing sellers to adjust or risk deals falling through.

Short-Term and Long-Term Resale Price Impacts When Incentives Rise

The immediate effect of increased builder incentives is a shift in buyer attention and foot traffic. Within weeks of a visible rate-buydown campaign or upgrade promotion, buyers who were browsing resale listings start requesting showings at new developments. Resale agents report fewer inquiries, longer gaps between showings, and buyers referencing builder offers during negotiations. This demand shift is most pronounced in markets where new and existing homes compete directly on price, location, and school access. Sellers who were receiving multiple offers in a tight market may suddenly see single lowball bids or no offers at all, forcing a reassessment of list price and strategy.

In the short term (zero to six months), resale values adjust through a combination of price reductions and increased seller concessions. Sellers initially resist cutting price, instead offering modest closing-cost help or including appliances. But if inventory continues to sit, more aggressive cuts follow. During this window, days on market for resale homes in incentive-heavy neighborhoods typically rise 15% to 30%, and the share of listings with price reductions climbs. In the medium term (six to eighteen months), the trajectory depends on absorption rates. If builder incentives successfully move inventory and new-home supply tightens, resale pricing can stabilize and even recover. If incentives persist because demand remains weak or builders continue adding inventory, downward pressure on resale values continues and can deepen.

Four signals that incentive-driven resale price pressure is intensifying:

- Persistent or expanding builder incentive programs. If rate buydowns and upgrade packages remain or increase in value quarter after quarter, it signals ongoing soft demand and sustained competitive pressure on resale homes.

- Rising new-home inventory alongside flat or falling sales. Inventory above six months’ supply combined with sluggish absorption rates means builders will continue aggressive promotions, prolonging resale pricing headwinds.

- Increasing share of resale listings with price cuts. When more than 30% to 40% of active resale listings in a submarket show price reductions, it indicates sellers are reacting to weakened buyer interest driven by new-build competition.

- Widening gap between list-to-sale price ratios for resale vs. new homes. If resale homes are selling at 95% to 97% of list while new homes close near 100% (before accounting for incentives), it shows buyers are negotiating harder on resale properties.

In the long term (eighteen to thirty-six months and beyond), resale values tend to track local employment, income growth, school quality, and overall housing supply constraints. If builder incentives were a tactical response to a temporary rate spike or seasonal slowdown, resale values typically recover once new-home inventory normalizes and incentives fade. But if incentives reflect a structural shift (like sustained oversupply of new homes, a regional migration reversal, or a prolonged period of elevated mortgage rates), the resale market may experience a lasting reset. Neighborhoods with continued high levels of new construction and aggressive builder pricing can see resale values remain depressed relative to pre-incentive norms, especially if buyers come to expect concessions as standard and appraisal comps reflect that new baseline.

Competitive Pricing and Concession Strategies for Resale Sellers Near New Developments

Resale sellers competing with incentive-heavy new construction need to focus on net-effective pricing, not just list-price positioning. When a builder’s offering a 2-point rate buydown, $10,000 in closing help, and $15,000 in upgrades, the resale seller has to calculate the buyer-facing value of that package and respond with an equivalent adjustment. On a $400,000 to $500,000 home, a competitive response often requires 1% to 4% in combined price reductions or seller concessions. Roughly $4,000 to $20,000. That can take the form of a direct price cut, which improves the home’s position in search results and attracts more buyer attention, or a package of closing-cost assistance and included items that mirrors the builder’s offer without changing the list price.

Offering closing-cost help of $5,000 to $15,000 is a common first step. Reduces the buyer’s cash requirement at closing and can be marketed prominently in the listing description. Funding a temporary mortgage buydown (like a 2–1 structure that reduces the buyer’s rate by two points in year one and one point in year two) typically costs 1% to 2% of the loan amount, or roughly $3,000 to $8,000 on a $300,000 to $400,000 mortgage. That creates a visible monthly-payment advantage that directly competes with builder-funded buydowns. Sellers can also invest $5,000 to $15,000 in targeted upgrades (updated kitchen countertops, new flooring, fresh exterior paint, or landscaping improvements) that close the perceived finish gap between the resale home and a new build without requiring a permanent price cut.

Five resale seller strategies to compete with builder incentives:

- Adjust list price by 1% to 3% to match net-effective builder pricing. Use recent builder sales data to estimate the total incentive value, then reduce your asking price by a comparable amount to position your home as the better deal on a net-cost basis.

- Offer buyer closing-cost assistance of $5,000 to $15,000. Advertise this in the listing to attract buyers who are cash-constrained and would otherwise be drawn to builder closing-cost credits.

- Fund a 2–1 or 1–0 temporary rate buydown. Work with your agent and a lender to structure a buydown that lowers the buyer’s payment in the early years, creating parity with builder rate-buydown offers.

- Make high-ROI cosmetic upgrades before listing. Focus spending on kitchens, baths, and curb appeal to neutralize the “new and shiny” advantage of builder homes and justify your asking price.

- Highlight resale-specific advantages in marketing. Emphasize mature landscaping, larger or more private lots, lower HOA fees, proximity to established amenities, and no wait time for move-in. Benefits that new construction often can’t match.

Agents should present adjusted comparable sales that account for builder incentive value when setting list price and negotiating offers. If three recent new-build sales in the neighborhood closed at a $450,000 contract price but included $20,000 in combined incentives, the net-effective comp is $430,000. Using the unadjusted $450,000 figure to justify a resale list price will result in overpricing, longer days on market, and eventual price cuts. Transparent, data-driven pricing that reflects the true competitive landscape builds buyer confidence and speeds the transaction, reducing carrying costs and the risk of further market softening.

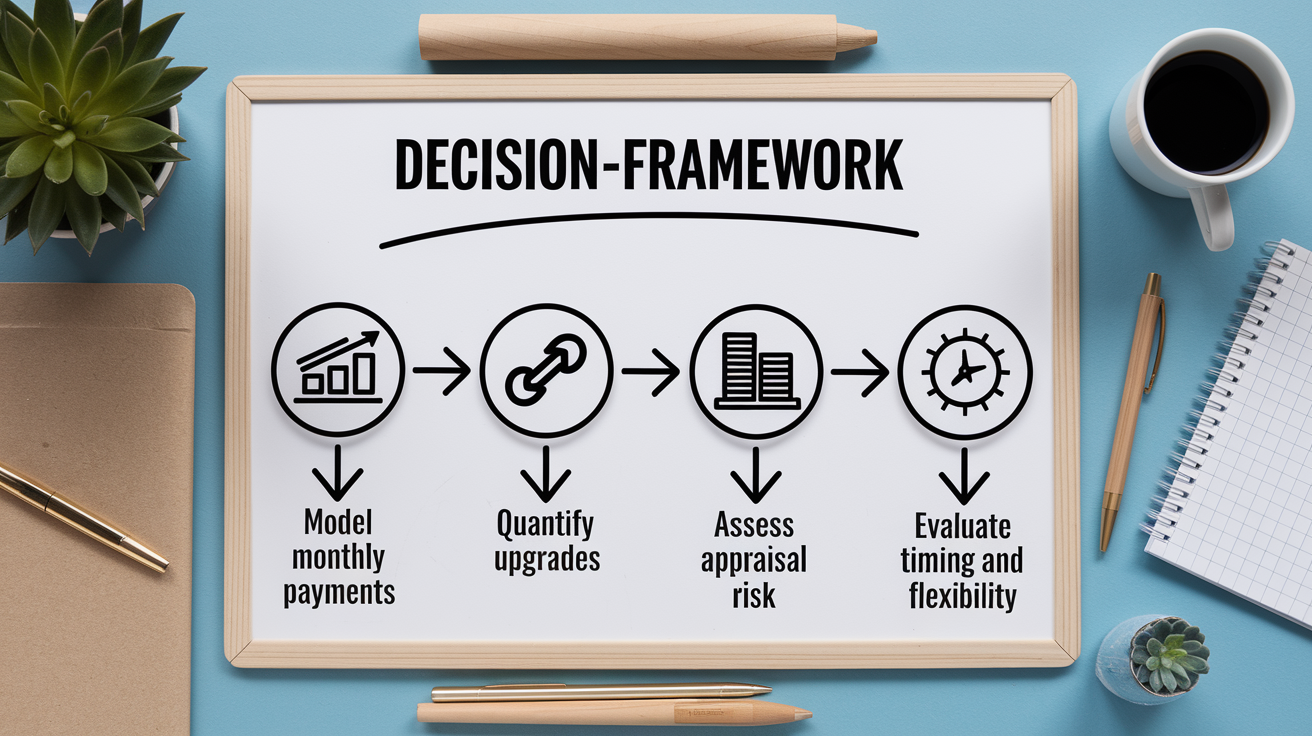

Buyer and Investor Decision Framework When Incentives Skew Market Pricing

Buyers evaluating resale homes against incentive-heavy new construction need to calculate total cost of ownership, not just compare list prices. The psychological pull of a builder’s package (lower monthly payment, reduced closing cash, included upgrades) can obscure the long-term financial picture. A new home with a temporary 2–1 buydown offers lower payments in years one and two, but the rate resets to market in year three. A buyer who plans to stay long-term needs to model the full payment schedule and compare it against a resale home purchased at a lower price with a stable, market-rate mortgage. Buyers should also verify whether builder incentives require using a preferred lender, which may limit their ability to shop for the best loan terms, and whether any incentives are contingent on waiving inspection rights or accepting other contract conditions.

Four steps buyers and investors should follow when evaluating resale versus new-build options under incentive conditions:

- Model monthly payments across the full loan term. Calculate the effective payment including any temporary buydown, then compare the blended cost over five, seven, or ten years against a resale home’s stable-rate mortgage.

- Quantify upgrade and concession value. Price out the cost of builder-included upgrades if purchased separately, and compare that to the cost of making similar improvements to a resale home. Often, builder upgrade packages carry higher margins than aftermarket renovations.

- Assess appraisal and resale risk. Consider whether the builder’s incentives will be reflected in future appraisals, potentially limiting your resale value, and whether the neighborhood’s resale inventory will remain under pressure if builder promotions continue.

- Evaluate timing and flexibility. New-build schedules can shift due to construction delays, while resale homes offer immediate possession. Weigh the value of certainty and control against the potential savings from builder incentives.

Investors face additional considerations. Builder incentives that lower the effective purchase price can improve cash-on-cash returns and cap rates in the near term. But if those incentives signal oversupply or weak demand fundamentals, future rent growth and resale liquidity may suffer. An investor buying a new rental property with a rate buydown and closing-cost help may enjoy lower initial debt service, but if the neighborhood’s resale values decline due to sustained builder competition, exit options narrow and equity appreciation slows. Investors should track local absorption rates, new-home permits, and the duration of builder incentive programs. Markets where incentives are short-lived tactical promotions present lower risk than markets where incentives have been standard for multiple quarters, suggesting structural demand weakness. Cash buyers and investors with shorter hold periods may find value in resale homes that have already adjusted price downward in response to builder competition, capturing the discount without exposure to future incentive-driven erosion.

Final Words

In the action, builder perks – rate buydowns, closing credits, and upgrade packages – shave the net-effective price of new homes and pull buyers away from resale listings.

That shifts comparable sales, can push appraisals down within 1-3 quarters, and creates short-term resale price pressure where new and existing prices sit close together.

The short answer to what increased new-construction incentives mean for resale prices is this: expect temporary price compression near active developments, faster seller adjustments, and clearer buying opportunities. Track inventory and net-effective comparisons — there’s opportunity if you move smart.

FAQ

Q: Do new construction homes have good resale value?

A: New construction homes have good resale value when they’re in strong locations, well-built, and competitively priced; builder incentives and nearby new supply can pressure resale, so compare net-effective price before deciding.

Q: What is the hardest month to sell a house?

A: The hardest month to sell a house is typically January, when buyer demand dips after holidays; seasonality and local climate matter, so winter months in your market are often the weakest.

Q: What is the 3-3-3 rule in real estate?

A: The 3-3-3 rule in real estate is a flexible agent heuristic: test a listing for 3 weeks, review buyer feedback after roughly 3 showings per week, and consider a 3% price adjustment if interest stays low.

Q: Are builder incentives worth it?

A: Builder incentives are worth it when they lower your net-effective cost without costly financing strings; always compare net-effective price, confirm appraisal treatment, and weigh trade-offs like required lender use or reduced negotiation.